Yesterday, we saw a decline in the major financial markets that brought the NASDAQ index close to bear market territory (down 20% from its recent all-time high) and the S & P 500 into correction territory (down 10% from its recent all-time high.

What poison were the empty heads in the toxic financial media spewing at investors? They were carping about the fact that the S & P 500 had its worst day since June 2020 and the NASDAQ (technology index) had its worst day since September 2020, while the DOW hit its lowest level in nearly 10 months.

This irresponsible “reporting” triggered and/or heightened the natural autonomous fight-or-flight response that human nature exhibits when confronted with perceived danger, which is to get out of harm’s way as quickly as possible. Investors do this by reflecting their fears in their portfolio strategy and selling their stocks into another TEMPORARY decline (history is devoid of one example of a decline in the S & P 500 that was not temporary). By taking this action, investors experience a permanent loss the only way possible -- humanly manufacturing it by selling into the temporary decline. A corollary loss is experienced by those who delay investing cash meant for long-term investment as they wish to wait for the “dust to settle.” These will likely be the most costly financial mistakes they ever make, mistakes from which they may never recover, in many cases irreparably jeopardizing their wealth and their ability to retire comfortably and to stay comfortably retired. For the ultra-wealthy, multigenerational wealth may be destroyed.

CONTEXTUAL FRAMEWORK FOR UNDERSTANDING RECENT MARKET CONDITIONS TO AVOID THESE IMMEASURABLY COSTLY MISTAKES

Let me start by saying that experiencing tremendous feelings of anxiety during market declines is only natural and such feelings should not be suppressed, BUT they should NEVER be reflected in one’s portfolio strategy by liquidating any portion of one’s stock portfolio in the belief that this is a protective strategy. It is quite the opposite – a destructive one! The research firm Dalbar (the leading firm that has been quantifying in an annually updated analysis for almost 30 years the actual cost to investors of their poor behaviors) finds that these market timing behaviors have cost investors to miss out on fully one-half of the returns available by simply remaining invested – a cost that often leads to financial failure.

What is really happening?

- The S & P 500 is down about 10% this year. This is a garden variety correction. JP Morgan’s research shows that since 1980 the average annual intra-year decline in the S & P 500 is about 15%. What we have experienced so far this year is a decline that would need to continue another 5% lower to simply be classified as average.

- We are in the first year and nascent stages of a Federal Reserve Interest Rate Hike Cycle. There have been 12 of them since 1954, and these cycles – from the first rate hike to the final one – have lasted between 2-to-3 years.

- The annualized returns for the stock market have been positive in all but one of the 12 cycles, meaning investors experienced robust returns during these cycles 92% of the time.

- The only period with negative returns was 1972-1974 when investors lost 8% annually for the period. The market is already down more than that this year. This period was marked by one of the worst economic climates in modern history with an historic oil crisis, a slowing economy and with interest rates, unemployment, and inflation all at or near 20%. Our economy is presently growing at historically high rates and interest rates, unemployment and inflation are a fraction of what they were in the ‘70s.

- The average annual return for the S & P 500 during the 12 rate hike periods exceeded 8%. Therefore, from current levels, the market would need to increase by about 18% by year-end from yesterday’s close to reflect the average during these cycles.

STILL NOT FEELING BETTER? WELL, THIS SECTION SHOULD HELP!

Herding or following the crowd has consistently resulted in poor investment decisions that lead to bad and often life-altering outcomes. Unfortunately, human nature prefers to fail conventionally (following the crowd) than to succeed unconventionally (unable to act alone on the courage of their convictions). The herd’s high level of current pessimism indicates that healthy returns likely lie ahead.

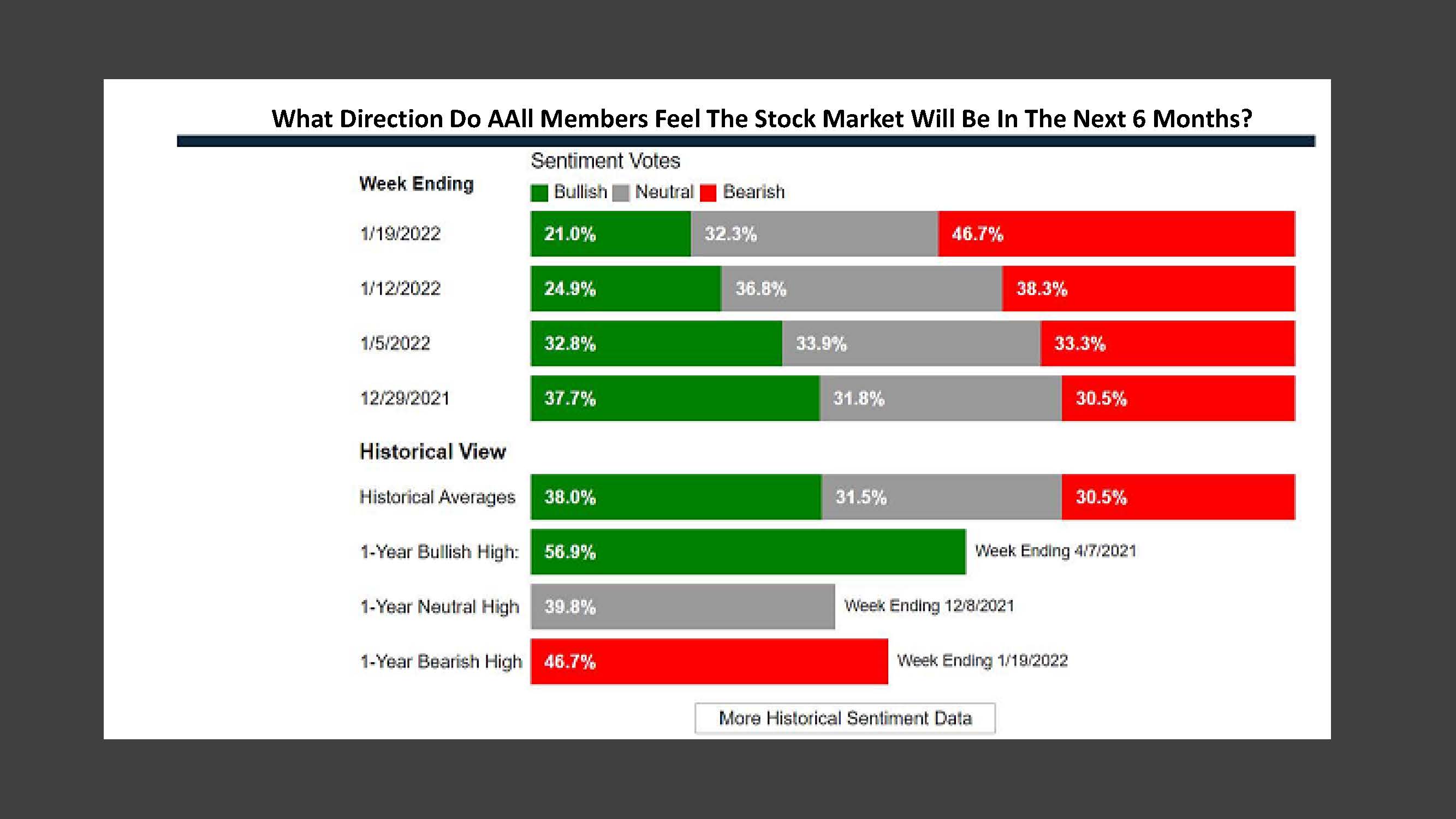

The American Institute of Individual Investors (AAII) publishes a weekly survey every Wednesday that measures investor sentiment. The most recent survey for the week ended 1/19/22 revealed the following:

- Bullish sentiment (expectations that stock prices will increase over the next 6 months) fell to 21%, its lowest level in 18 months – levels last seen around the market bottom during the COVID-related investor panic. The market is up 32% since then!

- In the nearly 4 decades since the AAII survey began being published, whenever bullish sentiment was lower than 28%, THE AVERAGE GAIN OVER THE FOLLOWING 6 MONTHS WAS OVER 8%. The current historically low reading of 21%, combined with the fact that we are in the beginning of the Fed Rate Hike Cycle, bodes very well for patient (i.e., well-behaved) investors.

- Bearish sentiment (expectations that stock prices will fall over the next 6 months) is currently at a historically high level of 47% (50% above the nearly 4-decade average bearish reading of 30%). Pessimism at these levels was last seen during the COVID-Panic around 18 months ago when the market was 32% lower. Again, the herd was and almost always is, wrong!

THE BEST NEWS OF ALL

As Fusion has been counseling clients for the better part of the past decade, we believe strongly that we are in the third secular bull market (strong upward market lasting about 20 years) which began in March 2009. These bull markets never end on anything other than frenzied, greed-based euphoric buying of stocks in the complete absence of any kind of fear other than the fear of missing out (FOMO). Sentiment is – as it has been for much of this greatest bull market in history – at historic levels of pessimism and fear. In our June 22, 2017 newsletter, Why The Markets Can’t Go Higher, we told our investors that we were in the bottom of the 2nd inning of this most-hated and feared secular bull market. At that point, the S & P 500 was 2,434 and is now close to double that level in just over 4.5 years. We opined then that the S & P likely had thousands of points and many years to go before the end of this secular bull. Today we are likely in the bottom of the 4th inning, and we now say again that this secular bull likely STILL HAS THOUSANDS MORE POINTS AND A MAJORITY OF THIS DECADE TO GO BEFORE IT RETREATS. We will, of course, continue to experience normal corrections and shallow and / or short-live bear markets (as the COVID decline demonstrated, having recovered fully in about 6 months). Remember, history teaches that the declines are temporary, and the increase is permanent.

Bull markets are born on pessimism (March 2009), grow on skepticism (the past 12+ years), mature on optimism (not present yet in cycle) and die on euphoria (likely years away).

……..Sir John Templeton

Until our next dose of behavioral investment counseling “vitamin C,” stay calm and carry on. Your wealth and your family’s long term financial future are depending on it!

Wishing everyone the best of health and happiness for the New Year.