HAVE YOU BEEN SURPRISED BY THIS YEAR’S STRONG MARKET PERFORMANCE?

If the answer is yes, then you might not have read our past newsletters.

Fusion’s 2022 year-end Newsletter reminded readers that since 1950, prospective returns following S & P 500 declines of at least 25% have generally been exceptional for 1–10-year periods. The 2022 bear market decline reached 25% (when it fell to 3,577) in October. Just about nine months later, at 4,505, the S & P 500 has increased by 26%. Our April newsletter highlighted the near-record low sentiment among professional fund managers and how historical data shows that future returns tend to be above average following low sentiment readings.

Despite these positive indicators, many highly regarded Wall Street analysts were advising investors to reduce stock exposure and to expect further significant declines. However, these forecasts have proven to be unreliable time and time again. Studies show that expert forecasts have about a 48% accuracy rate, a little worse than tossing a coin!

Mike Wilson and David Kostin, Chief Equity strategists at Morgan Stanley and Goldman Sachs, respectively, each warned investors to sell stocks and expect a decline in the first half of 2023 of 20% or more to as low as 3,000 on the S & P 500. Those who followed their “advice” find themselves with potential permanent losses. The cost of market timing is much higher than it appears. For every $1 million either liquidated or withheld from being invested since last October, 20% ($200,000) or more has been missed. However, if that $200,000 was earned and left to compound at 8%, it would be close to $1 million in 20 years, $2 million in 30 years and so on. For longer periods and multigenerational wealth, the loss is staggering.

“It is tough to make predictions, especially about the future.”

~ Yogi Berra

WHY ARE MARKET FORECASTERS STILL IN BUSINESS?

Investors are often drawn to financial news and expert forecasts because we have a natural desire for certainty in an unpredictable world. However, uncertainty is a constant condition. The idea that certainty can be higher at one point in time than another is misleading. On September 11, 2001, uncertainty in the world did not increase. The risk of a terror attack was probably as certain as it had ever been the day before, on 9/10. We were just oblivious to that risk. Certainty levels hadn’t changed on 9/11. What changed was our level of ignorance to the risk. Our illusion of certainty was challenged.

According to Daniel Kahneman, the Nobel Prize winning father of behavioral economics, one reason we continuously listen to forecasts, study history, and watch the news is to feed our hindsight bias. The ability to explain the past (hindsight) or try to divine the future relative to the past gives us the illusion that the world is understandable.

We have a love affair with the illusion of certainty and the illusion of control which clouds our judgment with respect to rational decision making. The less control we have of something and the larger the stakes of the outcome, the more willing we are to listen to just about anyone with any apparent authority or knowledge of the subject matter.

Ultimately, the illusion of control is more appealing to us than the reality of uncertainty.

~Daniel Kahneman

HOW DOES THE BROAD WEALTH MANAGEMENT INDUSTRY GENERALLY ADDRESS UNCERTAINTY?

The industry generally hands investors back the illusion of certainty that they seek. This is why the industry employs thousands of economists and analysts and markets those “capabilities” to investors. It is also why mutual funds are ranked by a star system. The Morningstar star system is based on ranking funds with the best past performance the highest. In reality, Funds tend to experience long periods of underperformance following long periods of out-performance. Ironically, once a fund receives five stars it is more likely to underperform than to outperform.

People tend to be willing to listen to those who seem to be telling them what they want to hear, even if they are consistently wrong. We are attracted to good-sounding advice when what we need is good advice. The two are often mutually exclusive.

WHAT IS AN INVESTOR TO DO?

Fusion is proud to counsel investors to embrace uncertainty and to learn how to make rational money decisions given constant uncertainty. We help to identify biases and modify the investment behaviors they induce. Here are some important guidelines and helpful observations:

1. A good bet in economics is that the past wasn’t as good as you remember, the present is not as bad as you think, and the future will be better than you anticipate.

2. Understand that the implacable enemy of investors is NOT market fluctuation, but rather, the long-term extinction of purchasing power (the inability to have your dollars keep up with the cost of living (inflation). Stocks have historically grown assets and dividends dramatically higher than inflation. Bonds freeze income and assets in the face of inflation. Investments that lead to the growth of our purchasing power are safe and those leading to the destruction of our purchasing power are risky. To the multi-decade and multi-generational investor, stocks are safe, and bonds are risky.

3. Bonds and cash should play a role, just not the industry’s suggested role of limiting temporary declines. Bonds and cash in an amount equal to 2-3 year’s living expenses enable investors to avoid dipping into their stock portfolio for spending during periodic market declines. This leads to maintaining appropriate critical exposure to the inflation- fighting, permanent long-term returns of stocks.

4. The goal is never to try to identify what will likely be the highest returning investment over the next year or two. The goal is to identify the best returns that you can sustain for the longest period. The biggest and most obvious secret in investing is that average returns earned for an above average period leads to extraordinary results. The common denominator of most big fortunes is not returns, but endurance and longevity. Warren Buffet generated over 90% of his ($130 billion+) fortune after age 65. When Amazon’s Jeff Bezos asked him how he had achieved such great wealth, he said: “by getting rich slow, nobody wants to get rich slow.”

5. We are more sensitive to changes in the value of our portfolio than to the overall portfolio value itself. We tend to be much more interested in comparing the value of our portfolio to its value 10 months ago, or 10 minutes ago, rather than 10 years ago. While we want to suppress volatility, it is far more important to suppress the urge to watch our portfolio too often. We tend to be obsessed with strategies that minimize the short-term changes in the value of our portfolios even though these strategies tend to also minimize the overall long-term value of our portfolios (i.e., too much bond exposure, market timing, etc..).

6. BE HAPPY!

“If only we wanted to be happy, it would be easy; but we want to be happier than other people, which is always difficult, since we think them happier than they are.”

~Charles de Montesquieu

Wishing everyone a happy, healthy, and fun summer.

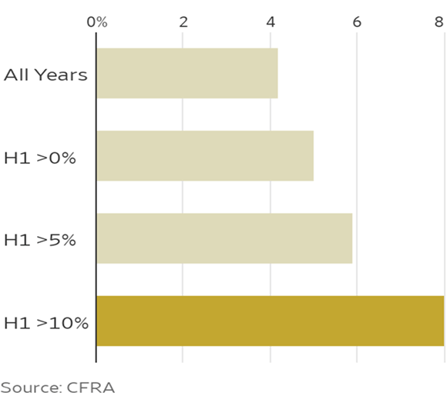

P.S. There will likely be many negative media narratives that will center on the theme that the market is too high and that is has come too far too fast and is therefore due for a big decline. Nobody knows the direction of the next 20% market move, but here is some historic context. Since 1945, when the market’s return in the first half of the year has been at least 10%, the market is positive in the second half of the year 82% of the time and gains 8% more, on average.

S & P 500 average performance during second halves since 1945