Our prayers and thoughts go out to all the Ukrainians as they are forced to defend their homeland in the face of unprovoked aggression and to face an unimaginable humanitarian crisis.

I write this newsletter with a heavy heart as a human being and as a direct descendant of my Ukrainian-born grandfather, Morris Kossar, who fled Kyiv from pogroms in the early 1900s and brought the Bialy to America – founding the famous Kossar’s Bialys on Manhattan’s lower east side. (https://gothamist.com/food/the-explosive-history-of-kossars-nycs-most-famous-bialy-bakery)

The Bialy comes from Bialystok in Poland. Its official name is Bialystoker Kuchen, which literally translates to “bread from Bialystok.” But for my grandfather’s common sense, bravery, grit and extremely good luck, I might now be faced with the task of taking up arms to defend my home country instead of having the privilege and good fortune to help families protect and grow their wealth.

So, before I share the contextual framework that may help you understand the likely impact of this crisis on your investment plan, a seemingly much more mundane issue relative to what the Ukrainians are now facing, let’s all say a prayer for these brave and strong human beings.

The History of Global Crises Involving War

While history is not ever a precise guide to understanding our future, it is often the best and only guide there is.

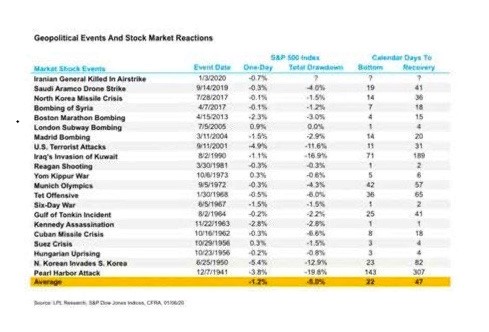

We looked at 21 such crises beginning with the attack on Pearl Harbor in 1941. With respect to the most extreme event I hear investors stating they fear, – nuclear war between US and Russia – the most analogous crisis among the 21 seems to be the Cuban Missile Crisis in 1962 when Russia positioned nuclear missiles in Cuba, 90 miles from the US. The S & P 500 declined a total of 6.6% before bottoming out 6 days after the crisis began and it had fully recovered 18 days after the crisis began. The average market decline considering all 21 events was 5%, which was reached, on average, 22 days after the event and the market’s average time to full recovery was about 1.5 months from the onset of the crisis.

TODAY MARKS THE 22nd DAY OF RUSSIA’S INVASION OF UKRAINE – WHERE ARE WE RELATIVE TO HISTORY?

The high for the S & P 500 was 4,294 on February 24, the day of the invasion. It bottomed out on March 8, closing down about 3% at 4,170. The market closed yesterday at 4,357 which is up about 1.5% since the invasion. NOTE: WHILE THE MARKET IS DOWN ABOUT 10% FOR THE YEAR, NONE OF THAT DECLINE OCURRED AFTER WAR BROKE OUT, BUT RATHER IN RESPONSE TO INFLATION AND RATE-HIKE FEARS.

So far, history appears to have proved a reasonable guide for contextualizing market expectations. The war and its global economic impact is very fluid, but generally, this is how the market reacts in response to such events. The ones we are living through always feel worse than past similar events because we know how those events were resolved and we never can know the outcome of a current crisis. We often view current crises as unprecedented events and I suppose each new one sets some new precedents relative to past similar events. However, as I pointed out in our September 27, 2021 newsletter – Shouldn’t We Protect Our Portfolio Against a Market Downturn at These Levels? – unprecedented is defined as something that has never happened or existed before. The American investor mistakenly thinks it means something that poses an insoluble problem that will permanently impair the value of their investments and lead to financial ruin. Remember that things that have never happened before like Y2k, 9/11, Brexit, Coronavirus, etc.. happen all the time. As I have said many times, it is human to feel anxious and afraid during times like this, but it is absolutely financial suicide to reflect these fears in our portfolio strategy by selling our temporarily discounted investments. Waiting for the proverbial “dust to settle,” which means waiting for more perceived certainty before we reenter the market means we will be selling low and buying high. This is the opposite of what we must do to preserve and grow our wealth consistently over time.

CONSISTENCY IS THE KEY TO SUCCESS

Human nature, which is always and everywhere a failed investor, is programmed to exhibit fight or flight responses to stimuli. When markets decline our flight response is to want to sell our stocks. We may get lucky (very rarely) acting on our impulse to exit stocks before a major market decline. However, while the impulse to flee is innate in all of is, it is just an impulse, because getting out is at best half a strategy. In the absence of a strategy for re-entry, one will just wait until they feel the impulse to get back in. The odds that these two impulses, acting in sequence, will yield better results than simply riding out the full volatility of all the ups and downs are prohibitive to the point of impossibility. The ONLY way to hope to experience the fullness of the long-term returns available in stocks (10% annually for the past 90+ years) is to be willing to ride out the full volatility, period!

Consistency in ALWAYS acting on one’s plan and NEVER reacting to the markets, short-term performance, the media, and current events is the only approach that will allow families to truly preserve and grow their wealth. NEVER sing the four word death song of the American investor – “THIS TIME IS DIFFERENT” to justify malignant investor behaviors like attempting to time the markets. The dramatic costs of such behaviors are well documented and can be revisited in the “what is the cost of trying to exit stocks before corrections/bear markets/recessions” in our September 27, 2021 newsletter, Shouldn’t We Protect Our Portfolio Against a Big Market Downturn at These Levels? Practicing the right behaviors will not ALWAYS yield desired short-term outcomes, BUT CONSISTENTLY MAKING THE RIGHT DECISIONS OVER AN INVESTOR’S LIFETIME HAS THE HIGHEST PROBABILITY OF YIELDING THE BEST LONG-TERM OUTCOMES, BY AN EXTREMELY LARGE MARGIN.

IT IS NEVER THE KNOWN UNKNOWNS

Donald Rumsfeld’s career in public service was so long that he is both the youngest and second oldest to have ever served as secretary of defense (’75-’77 - under Gerald Ford and ’01-’06 - under “Dubya”). His operating hypothesis was that in his job he would always have to be dealing with unknowns. But he said the unknown breaks down into two categories: known unknowns and unknown unknowns or “black swans, and it isn’t the known unknowns that get you”

"...And it isn’t the known unknowns that get you."

Donald Rumsfeld

Outbreak of war is one of the most common known unknowns. We know we have the conflict, but don’t know what the effects will be globally and how/when it will be resolved. While the media always likes to carp about how much the market hates uncertainty, the very concept is completely ridiculous. Prior to a war’s outbreak, we have maximum uncertainty (as we have no idea if or when the war is coming) and stock prices do not reflect the fullness of potential negative outcomes related to an event before it existed. Once the war breaks out, there is more, not less, certainty in that the prices of companies adjust to reflect potential negative consequences like a spike in the price of energy and the impact on future earnings.

Other examples of current known unknowns are the current multiyear interest-rate hike cycle we have just entered and the spike in inflation, both of which we can be pretty sure the market has priced in. An example of unknown unknowns in recent history are 9/11 and the single-family American home causing the near collapse of the global financial system in 2008 and most recently the 2020 pandemic. We have not experienced deep, and/or prolonged bear markets related to the known unknowns, as the market digests the data and adjusts pricing accordingly. Conversely, the black swans like 9/11, the ones we can’t see coming at all, are the ones that cause long/protracted or deep bear markets. It has always been that way and for logical reasons. With respect to those fearing nuclear Armageddon, it is critical to understand that one cannot marry a financial plan to apocalyptic speculation. And, as Art Cashin said, “Don’t bet on the end of the world ‘cause it only happens once and something that only happens once in infinity is a long shot.”

“Don’t bet on the end of the world ‘cause it only happens once and something that only happens once in infinity is a long shot.”

Art Cashin

Uncertainty is the condition of observing something that may or may not happen. The future, by its very nature, is uncertain. As investors -- who are investing our capital for some future use – we must deal with that uncertainty in our decision-making. Therefore, successful investing must not be characterized as the ability to consistently predict or time the market (things that neither we nor anyone else can consistently do) but rather by practicing rationality under uncertainty. Going to cash in response to one or more current events or in response to geopolitical, economic or market uncertainty is a classic example of irrationality under uncertainty. This is because creating such a portfolio (going to cash) as a response to uncertainty must be premised on the certainty of imminent economic and/or financial collapse. The irrationality is that we are discounting the possibility of disaster (the uncertainty of it) by creating a portfolio entirely based on the certainty of disaster. Those who reflect their fear of Armageddon by selling their investments and going to cash have always and only created their own financial Armageddon, causing them to fail to reach their most important financial objectives, to lower their quality of living, greatly diminish their financial legacy to children, and in the worst case, to actually run out of money! AT FUSION, WE DO NOT DO ARMAGEDDON!

POSITIVE MARKET CLIMATE CONTINUES

In closing, I remind everyone that in all but one of the past 12 interest rate-hike cycles the market has performed very well averaging almost 9% annually during the 3 years of a rate-increase cycle. We are in the 13th year of the third and greatest secular (two decade-long) bull market. Investor sentiment is near record lows and at about $20 trillion, investor cash levels are near historic highs (historically, a winning combination for future stock prices). All of these bode very well for equity investors. Moreover, we are in the beginning stages of the most powerful economic megatrend in generations – the movement of 12 million people per month from poverty into the global middle class (Primarily in India and Asia)– which will likely create a long and robust global economic consumer-driven expansion for many years to come. Finally, these great secular bull markets never end on fears of war, election outcomes, tariffs, pandemics, etc… They only end on the fear of missing out (FOMO) when investors increasingly unleashing their cash on the next dotcom-like bubble. We are nowhere near that point and real fear is as palpable as it has been in a long time. There is likely a long runway ahead before we see the next bubble forming. Until then, we continue to march.

WHAT AN EXCITING TIME TO BE A GLOBALLY DIVERSIFIED EQUITY INVESTOR!!

Wishing everybody a safe and happy Spring. And, the next time you eat a bialy, please think of grandpa ‘Moe,” AKA “THE BIALY KING!”